Set to revolutionize various industries, blockchain technology is gaining widespread acceptance. However, the misunderstanding surrounding the technology is such that it is being falsely interpreted to be a messiah of sorts.

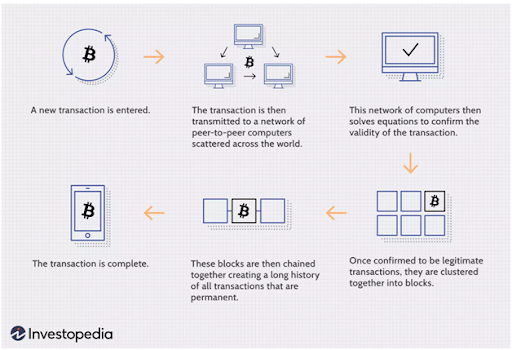

A blockchain is a publicly available ledger that is used to log transactions. As the name suggests, blockchains are made up of blocks of data that are linked to each other. A new “block” created within a blockchain to record a transaction contains the address or the link to the last block in the blockchain, thereby creating a “chain”. Each block contains the following – a link to the previous block, timestamp and the actual data. The timestamps represent when a particular block was added and these cannot be modified by anyone. The data stored within the blocks could be anything. In terms of cryptocurrency, the data represents the actual value of a remuneration being paid for some service that was received.

Blockchains essentially have three major properties that make them popular – they are distributed, highly secure and are publicly available. As blockchains are distributed, the files or logs that represent transactions are stored at multiple locations on various computers. Blockchains aren’t under the control of one person or an organization because of this distributed nature and cannot be edited or deleted by those wanting to do so, unless all who are part of the blockchain agree to such a modification.

Security is ensured through the implementation of cryptography where the blocks themselves are encrypted and require keys in order to access that particular block’s information. The data is immutable and the timestamps of these blocks cannot be tampered with.

Due to its public nature, the transactions are transparent and accessible by anyone (anyone who needs to have access to the blockchain). This adds an extra layer of security to the blockchain as all the users can monitor changes made to the blockchain at any time.

Some of the current applications of blockchain that most aren’t aware of include using them to trace the origin of diamonds and where they are headed, track where shoes were manufactured and who made them so that the customer would know if what he pays for the final product reaches the maker, maintaining records at government offices, verifiable credentials and tracing and tracking the origin and the path of goods. Some of the more common applications of blockchain include cryptocurrency, food industry, healthcare, real estate, insurance and supply chain, among others.

Click here to know more about cryptocurrency!

Now that we have seen the applications of blockchain, let’s take a look at the different career opportunities in blockchain that are associated with it.